-

05 Mar Off

| Social Security encompasses retirement benefits, disability benefits, and is intertwined with Medicare benefits. This guide focuses on Social Security retirement benefits, the most common association of the term Social Security. There are currently more than 50 million people receiving Social Security retirement benefits (i.e., Old Age and Survivor Insurance or OASI). Social Security Employment Tax Minimum Eligibility Requirements How Benefits Are Calculated How to Find Out Your Own Benefit Information Taxes on Benefits

Spousal Benefits

Spousal Benefits for Divorcees Survivor Benefits Cost of Living Adjustment (COLA)

|

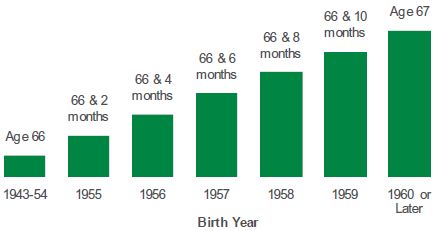

Full Retirement Age Your Full Retirement Age (i.e., the age that you qualify to receive full benefits), depends on the year you were born. The chart below shows the full retirement ages by year of birth.

Early or Delayed Social Security Benefits Percent of Full Retirement Age Benefit

Taking Early Benefits While Continuing to Work Recent Legislation Potential Future Legislation When to Take Social Security How to Apply |

Related Articles

Comments are closed.